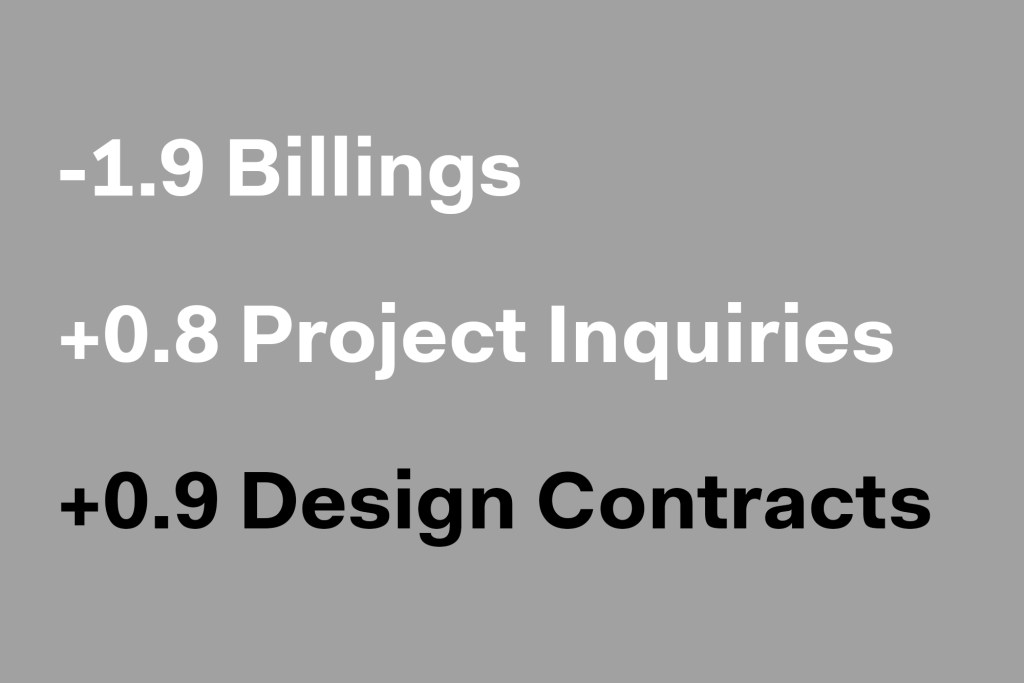

The American Institute of Architects monthly Architecture Billings Index posted at 48.5 in April, contracting 1.9 points from March’s score of 50.4 and dipping back below 50.0. The ABI is a leading economic indicator of construction activity in the U.S. and reflects a nine- to 12-month lead time between architecture billings and construction spending nationally, regionally, and by project type. A score above 50 represents an increase in billings from the previous month, while a score below 50 represents a contraction.

“The uncertainty in the economy is permeating into many sectors, including architecture.,” says Ali Wolf, the chief economist of ARCHITECT’s parent company, Zonda. “Among architecture firms, those focused on multifamily are feeling a more pronounced slowdown than commercial/industrial and institutional, for example. This slowdown is a result of tightening access to credit, higher rates, and a difficulty getting new deals to pencil.”

The scores for project inquiries and design contracts were mixed in April. New project inquiries posted at 53.9, rising 0.8 point from March’s score of 53.1. Design contracts remained contracted in April with a score of 49.8, increasing 0.9 point from March’s score of 48.9.

“The ongoing weakness in design activity at architecture firms reflects clients’ concerns regarding the economic outlook,” said AIA chief economist, Kermit Baker, Hon. AIA, in a press release from the organization. “High construction costs, extended project schedules, elevated interest rates, and growing difficulty in obtaining financing are all weighing on the construction market.”

The month-to-month changes in scores for regional billings—which, unlike the national score, are calculated as three-month moving averages—remained flat in April, with one score remaining above 50.0. Billings in the Midwest fell 0.2 point to a score of 51.2, while billings in the West rose 2.1 points to a score of 49.3. Billings in the South increased 1.3 points to a score of 48.7, and billings in the Northeast fell 1.9 points to a score of 47.2.

April’s sector billings scores expanded slightly. The commercial/industrial sector rose 2.1 points to a score of 51.8; the institutional sector increased 1.8 points to a score of 50.6. The multifamily residential score fell 2.7 points to a score of 41.5, and the mixed practice sector fell 1.8 points to a score of 52.1. Like the regional billings scores, sector billings scores are also calculated as three-month moving averages.

Read more business news: March Billings Improve Slightly | Decline Slows for December Billings | Billings Slow Again in November | Moderated September billings reflect pressures in housing market